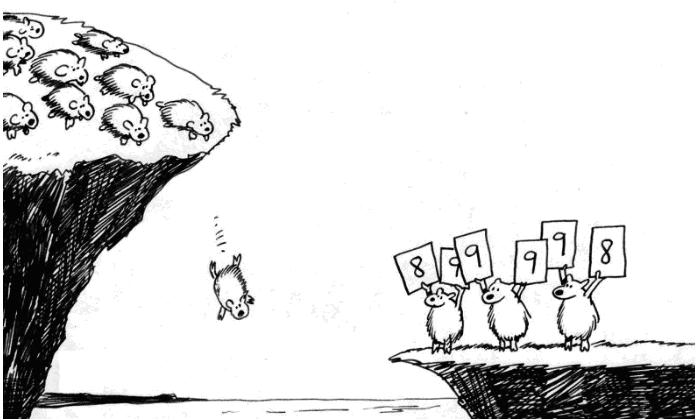

The perils of relative performance measurement

Intern Testimonials

What Coniecto’s interns had to say about the internship program after completion.

Investing in Crypto, the Warren Buffet way!

There are many different ways to gain exposure to cryptocurrencies.

How to be the BEST employer ever

Some of the things that we did to make the Coniecto Internship Program a success amidst the pandemic.

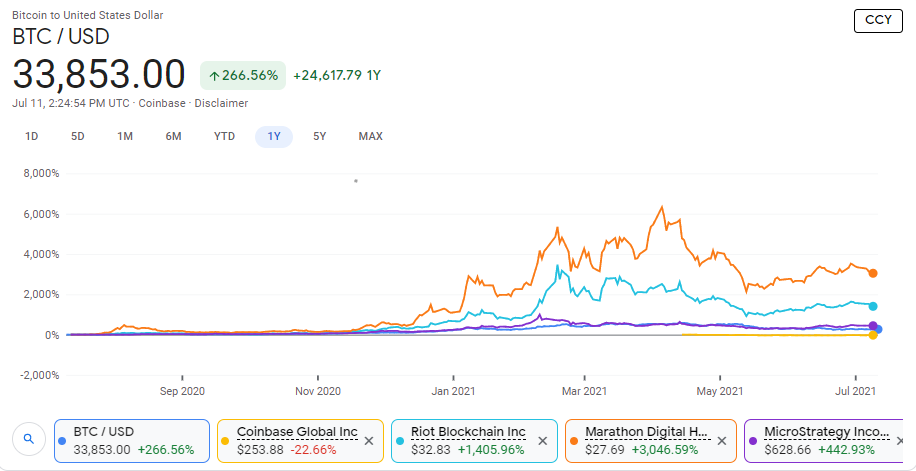

Is Bitcoin Still The Crypto-King?

While indicators for investing in the stock market tend to be metrics like acceptable P/E ratios and Interest rates, the case for an emerging and technologically defined market such as cryptocurrencies is different. An analyst from JP Morgan suggested the indicator for a Bull run for Bitcoin to be the coin’s market share as a…

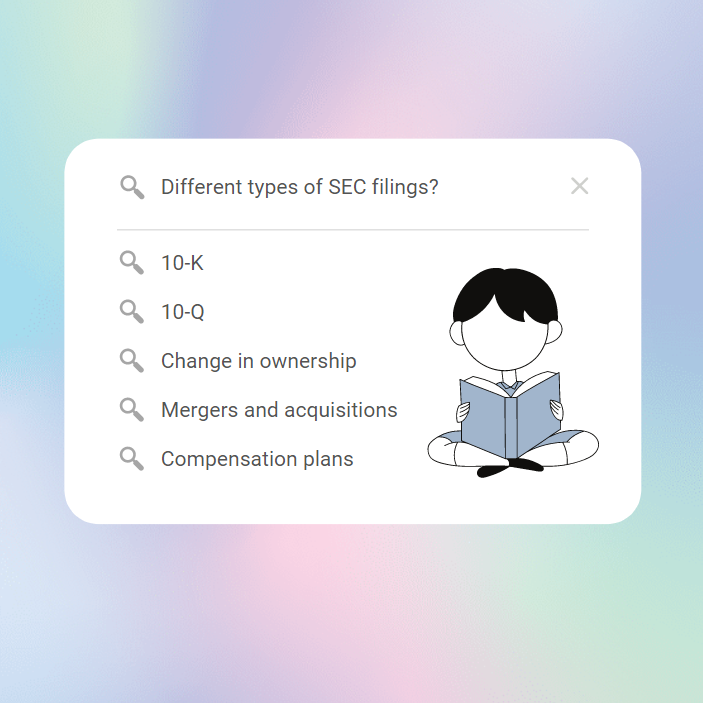

SEC filings – All you need to know.

Let’s learn! – What are the 10-Ks, 10-Qs that you hear of in the news? This guide is useful for beginners tracking the US markets.

Gender Sensitivity At The Workplace

There is equal opportunity at Coniecto. We encourage best practices at workplaces.

Whitepaper – Internship As A Service

This whitepaper sets out the unique value proposition of our concept.

Summer Internship Topics 2021

Cool internship project ideas – you can do these with us at Coniecto Investments.